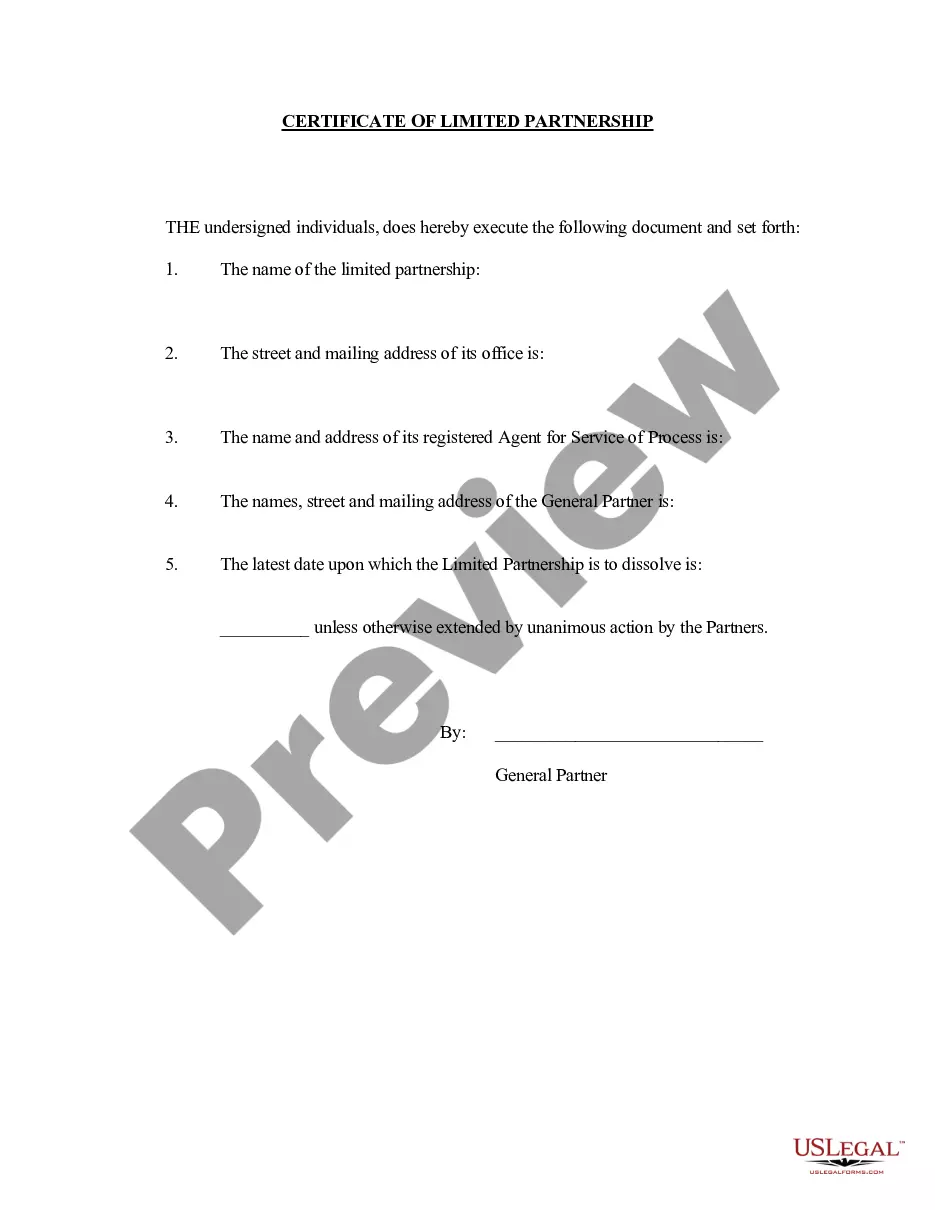

The partners agree to form a Limited Partnership pursuant to the provisions of the Limited Partnership Act. The partners agree to form a Limited Partnership pursuant to the provisions of the Limited Partnership Act. The general partner shall execute and cause to be recorded a Certificate of Limited Partnership and any additional documents as may be necessary or appropriate to form a limited partnership pursuant to state law. In Illinois, a Family Limited Partnership (FLP) Agreement and Certificate is a legal document that establishes and governs the operation of a family-owned limited partnership. This agreement outlines the rights, responsibilities, and obligations of the partners involved and provides a framework for the management and distribution of assets within the partnership. The Illinois Family Limited Partnership Agreement and Certificate are designed to provide unique advantages and benefits to families seeking to protect and manage their assets efficiently. By utilizing this type of partnership structure, families can reap various tax and estate planning benefits while enjoying asset protection and maintaining control over their assets. One type of Illinois Family Limited Partnership is the General Partnership. In this arrangement, the limited partnership is typically managed by one or more general partners who have unlimited liability for the partnership's obligations. The limited partners, on the other hand, have limited liability and are not involved in the day-to-day management of the partnership. Another type of Illinois Family Limited Partnership is the Limited Liability Partnership (LLP). An LLP is similar to a general partnership, but it provides limited liability protection to all partners, including general partners. This type of partnership is often favored by professionals such as lawyers, accountants, and architects. The Illinois Family Limited Partnership Agreement and Certificate include key provisions such as the partnership term, the allocation of profits and losses, the capital contributions required from partners, the rights and obligations of each partner, restrictions on partnership interests' transfer, procedures for admitting new partners, and dispute resolution mechanisms. Furthermore, this agreement also addresses key issues related to asset protection and succession planning. Families can use the FLP structure to protect their assets from potential claims, lawsuits, and creditors while maintaining control and management of those assets within the family. When creating an Illinois Family Limited Partnership Agreement and Certificate, it is essential to consult with legal professionals experienced in partnership laws and estate planning. They can help ensure that the agreement is tailored to the family's unique needs and goals, ensuring compliance with Illinois state laws and maximizing the potential benefits of utilizing this partnership structure. Overall, an Illinois Family Limited Partnership Agreement and Certificate provide families with a powerful tool for asset management, tax planning, and protection. By establishing clear guidelines and provisions through this legally binding document, families can secure their assets and pave the way for a smooth intergenerational transfer, ultimately safeguarding their family's wealth and legacy.

In Illinois, a Family Limited Partnership (FLP) Agreement and Certificate is a legal document that establishes and governs the operation of a family-owned limited partnership. This agreement outlines the rights, responsibilities, and obligations of the partners involved and provides a framework for the management and distribution of assets within the partnership. The Illinois Family Limited Partnership Agreement and Certificate are designed to provide unique advantages and benefits to families seeking to protect and manage their assets efficiently. By utilizing this type of partnership structure, families can reap various tax and estate planning benefits while enjoying asset protection and maintaining control over their assets. One type of Illinois Family Limited Partnership is the General Partnership. In this arrangement, the limited partnership is typically managed by one or more general partners who have unlimited liability for the partnership's obligations. The limited partners, on the other hand, have limited liability and are not involved in the day-to-day management of the partnership. Another type of Illinois Family Limited Partnership is the Limited Liability Partnership (LLP). An LLP is similar to a general partnership, but it provides limited liability protection to all partners, including general partners. This type of partnership is often favored by professionals such as lawyers, accountants, and architects. The Illinois Family Limited Partnership Agreement and Certificate include key provisions such as the partnership term, the allocation of profits and losses, the capital contributions required from partners, the rights and obligations of each partner, restrictions on partnership interests' transfer, procedures for admitting new partners, and dispute resolution mechanisms. Furthermore, this agreement also addresses key issues related to asset protection and succession planning. Families can use the FLP structure to protect their assets from potential claims, lawsuits, and creditors while maintaining control and management of those assets within the family. When creating an Illinois Family Limited Partnership Agreement and Certificate, it is essential to consult with legal professionals experienced in partnership laws and estate planning. They can help ensure that the agreement is tailored to the family's unique needs and goals, ensuring compliance with Illinois state laws and maximizing the potential benefits of utilizing this partnership structure. Overall, an Illinois Family Limited Partnership Agreement and Certificate provide families with a powerful tool for asset management, tax planning, and protection. By establishing clear guidelines and provisions through this legally binding document, families can secure their assets and pave the way for a smooth intergenerational transfer, ultimately safeguarding their family's wealth and legacy.